It is calculated by taking the total cha. The marginal cost of these is therefore calculated by dividing the additional cost 20000 by the increase in quantity 25000 to reach a cost of 080 per unit.

Econ 150 Microeconomics

Servicing one additional customer would cost 2000.

. Cost push inflation is typically depicted graphically as an a. Total production cost marginal cost per additional unit x total additional units This is the same as c x t p. Marginal cost is different from average cost which is the total cost divided by the number of units produced.

Less than the previous one to produce. For three units the marginal cost would be 10. Constant marginal costs occur when production of each individual unit costs.

C the same as the previous one. Heres what the formula would look like for calculating total production costs. The same as the previous one D.

Less than the previous one B. In this situation increasing production volume causes marginal costs to go down. Fixed costs of production are constant occur regularly and do not change in the short-term.

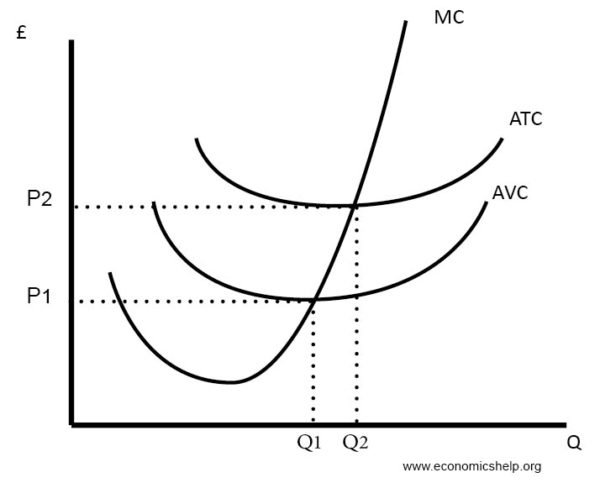

On a diagram draw the marginal cost curves for the two factories the average and marginal revenue curves and the total marginal cost curve ie the marginal cost of producing Q Q 1 Q 2. The same to produce as the previous one. Marginal cost is calculated by dividing the change in total cost by the change in the number of units produced.

More than the previous one. Constant returns to scale occur when the long-run average cost of producing each individual unit increases as total output increases. 61Constant marginal costs occur when production of each individual unit costs.

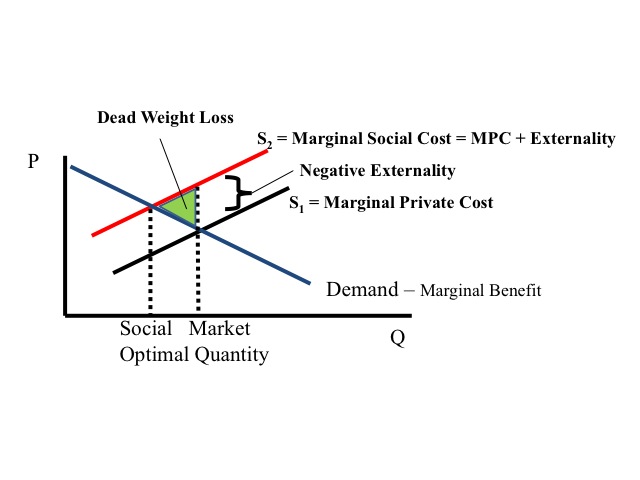

The total cost per hat would then drop to 175 1 fixed cost per unit 075 variable costs. The contribution is the difference between sales volume and the marginal cost of sales. The original market equilibrium is presented in the exhibit to the right with the supply curve S and the demand curve D.

Marginal Cost Change in Costs Change in Quantity Marginal cost represents the incremental costs incurred when producing additional units of a good or service. And so their marginal revenue curve it would just be a horizontal line that you see right over there and zero economic profit happens when you produce a quantity where your average total cost is the same as your marginal revenue. The market equilibrium price is Pe and the equilibrium quantity is Qe.

This trend would continue indefinitely because the cost of production per unit remains the same. In this example marginal costs for various activities exist. 100 2 Constant marginal costs occur when production of each individual unit costs.

Where the marginal costs would be 1005. The marginal cost for one additional unit produced is either 5 for any unit except the 101 st 201 st etc. B more than the previous one.

Marginal Cost Calculator This marginal cost calculator allows you to calculate the additional cost of producing more units using the formula. Example 3 Julie Porter owns a textile company that makes 200 dresses each year which costs 15000 to. Economies of scale A firm was producing 20000 units of output at the total cost of 40000.

Inward shift of the demand curve b. Fossils R Us Green House Oils Shale Ale Plant and property 900000 1500000 1000000 Extraction costs per barrel 45 31 40. The Law of Demand states that other things being constant an increase in the price of a good lowers the quantity demanded of that good while a decrease in the price of a good raises the quantity demanded of that good 48.

At each level of production and time period being considered marginal cost include all costs that vary with the level of production whereas. Lets say it costs 100000 to. For each unit the amount that you get which is that marginal unit thats also how much it costs you to produce it now remember when were.

Indicate the profit-maximizing output for each factory total output and price. The average revenue curve is the demand curve P 700 - 5Q. The entrepreneur estimates that average total costs per pack of dough would be 7 of which variable QA Consider the following cost structures for three oil producers.

Marginal costs are a function of the total cost of production which includes fixed and variable costs. Constant marginal costs occur when each individual unit costs A. More than the previous one to produce.

The perfectly competitive Shady Valley zucchini market can be used to illustrate a constant-cost industry. The first step in identifying the long-run industry supply curve for a constant-cost. The marginal cost of introducing a new product line would be 10000.

From this approach it is not possible to identify an amount of net profit per product but it is possible to identify the amount of contribution per product towards fixed overheads and profits. In marginal costing it is not possible to determine the profit per unit of product because fixed. More than the previous one C.

The same as the previous one. When will a firm find the optimal level of. A less than the previous one.

1 A farm can produce 1000 bushels of wheat per year with two workers or 1300 bushels of wheat per year with four workers.

Micro Chapter 8 Perfect Competition Flashcards Quizlet

Marginal Costs An Overview Sciencedirect Topics

Diagrams Of Cost Curves Economics Help

0 Comments